A Pre-Budget Overview of the Indian Economy – A Special Feature

|

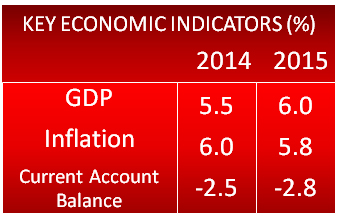

February and 0.5 percent in March 2014. March also saw a rise in inflation measured with the Consumer Price Index (CPI) at 8.31 percent. India's merchandise exports also contracted 3.15 percent to USD 29.6 billion.

April 2014 saw the first economic good news of the year with a 5.26 percent rise in exports followed by an increase in factory output with a 3.4 percent rise in IIP and a subsequent easing in inflation with the CPI slowing to 8.28 percent in May 2014. The formation of a new stable government in India led by Prime Minister Narendra Modi in May 2014 raised hopes of an upturn; several decisions and policies of the business friendly Modi government seem set to improve India's economic prospects, especially in the vital manufacturing sector. However, the Modi-led government that has vowed to focus on development has a formidable task ahead for its first budget session to revive the stuttering economy.

|

The total automobile market size in India is likely to triple from the present 1.7 million units to 9.3 million units by 2020. Driven by enhanced demand as the number of people with disposable income increases, the sector will grow at a compounded annual growth rate (CAGR) of 16 percent

during the period. The telecom sector is also forecast to gain with the number of telecom subscribers in India projected to grow from the current level of 898 million to 1.2 billion by 2016. Organized retail in India is estimated to grow more than 5 times from current level of USD 27 billion to USD 150 billion by 2020.

India's economic growth has been for decades hampered by its flawed economic policy. Economic empowerment needs the creation of new jobs in manufacturing and the modernization of agriculture. Micro, small and medium businesses contribute nearly 8 percent of India's gross domestic product (GDP), 45 percent of the manufacturing output and 40 percent of exports. Elevated inflation, a tight monetary stance and a weak currency will continue to constrain spending. Further, fiscal austerity is likely to be an additional drag on growth. Economic recovery will have to be led by improved investment and consumption. The opening up of foreign direct investment (FDI) in several sectors by the Modi-led government seems to be the right step in this direction. Modi also said recently that there is a need to administer "bitter medicine" to revive the ailing economy. Many structural reforms are expected in the finance sector, resulting in a stronger business sentiment, which can be thanked for the significant uptrend in the manufacturing and services sectors in June 2014. The HSBC Services Purchasing Managers' Index rose to a 17-month high of 54.4 in June from 50.2 in May. The HSBC India Composite Output Index, which covers both services and manufacturing, rose to a 16-month high of 53.8 in June from 50.7 in May. The growth momentum is expected to continue with faster reforms expected thanks to the political stability. However, although Modi may have laid the groundwork of positive economic growth for decades to come, the process could take longer than desired due to the nature of India's political system.

|

September monsoon is 10 to 15 percent below normal. A poor monsoon could also result in a 1–2 percent spike in the CPI.

Meanwhile, prices of petroleum products are steadily rising owing to changes in the international scenario, particularly the Syria–Iraq crisis. The increased fuel prices, the rising inflation and the poor monsoon are major factors to be considered as the new Indian government prepares its first Union Budget for 2014–15. This year's budget is probably the most crucial in recent times and will decide the economic trends in the years to come. A capitalist-favoring budget is being anticipated with measures helping entrepreneurial pursuits grow at large. At the same time, perks for middle and small-scale businesses will also help empower the economy.

(The above passage is a part of "Polymer Prospects based on Global Economic Indicators," a POLYMERUPDATE Special Report)

ABOUT POLYMERUPDATE

POLYMERUPDATE is a news and media portal headquartered in India that specializes in providing daily market-moving information and pricing data on petrochemical products and

industrial polymers from key markets in Asia, Europe, Middle East and the United States. The portal also hosts weekly and monthly scans on commonly used polymers and analysis reports based on import data in India in addition to the

POLYMERUPDATE/Platts Joint Reports on PE, PP and PVC.

POLYMERUPDATE mobile apps are currently available on iPhone and iPad, and BlackBerry and Android platforms.

POLYMERUPDATE also provides news alerts on the move through its SMS and instant messaging services. In addition,

POLYMERUPDATE publishes interviews and articles, which are a rich source of information on the latest trends in the chemical and petrochemical industry.

Visit POLYMERUPDATE on the internet at www.polymerupdate.com

Sign up for our newsletters

More like this

Troubled Iraq rattles oil markets, threatens economies – A POLYMERUPDATE Special Report Read More

An interview with GPCA's Dr. Abdulwahab Al-Sadoun Read More

Complementing Growth of Plastics Manufacturing in India: An Interview with UNIDO ICAMT Read More

Huntsman speaks with POLYMERUPDATE on its Polyurethanes Business and its Contributions to the Indian Plastics Industry Read More

ONGC Chairman Sudhir Vasudeva inaugurates Oil & Gas World Expo 2014 – A POLYMERUPDATE Report Read More

Connect with POLYMERUPDATE